The Math of No

FOMU isn't an emotion. It's a topology.

Roughly 40% of qualified B2B deals die without a competitor ever winning them — they end in no decision. This piece argues that the cause isn’t poor product, pricing, or messaging. It’s structural: the modern B2B buying group is a sealed network of stakeholders who can’t see into each other’s risk, and the cost of coordinating them grows with the square of the people in the room. FOMU — the Fear of Messing Up — is the symptom. Coordination debt is the mechanism.

Below: the data, the math, and what it means for how you sell into committees.

A champion walks out of a demo convinced. Six weeks later the deal is dead, and not one competitor touched it. No one said no. The deal simply never resolved.

This is the most common way B2B revenue dies in 2026, and almost every marketing budget is built to prevent the wrong thing.

The killer isn’t a rival. It’s a room.

Start with the number, because it reframes everything that follows. Across the research now circulating among revenue teams, roughly 40% of qualified B2B deals end in no decision — not lost to a competitor, lost to inaction. Some studies put the no-decision share of all lost deals between 40 and 60%. One analysis of millions of sales conversations found the same band. Whatever the exact figure, the direction is settled: your fiercest competitor is the status quo, and it wins more than anyone on your shortlist.

LinkedIn and Bain gave the feeling a name this June — FOMU, the Fear of Messing Up — and showed it consistently outweighs FOMO in business buying. Buyers aren’t primarily afraid of missing the best product. They’re afraid of being the one held accountable when something breaks.

Naming the fear is useful. But a name is not a mechanism. FOMU isn’t a mood that better copy can dispel. It’s the subjective readout of a structure — and once you see the structure, the 40% stops being a mystery and starts being arithmetic.

The asymmetry that runs the room

Begin with one person, because the logic compounds from there.

The procurement lead who approves a new vendor that underperforms absorbs the scrutiny, the blame, the career cost. The one who renews the incumbent absorbs nothing. Same uncertainty, wildly different downside. Saying yes is a wager against your own reputation; saying nothing is free. Rational individuals, facing that asymmetry, default to delay — and delay, repeated across a group, is indistinguishable from a no.

And the room is full of these wagers. Roughly 79% of B2B purchases now require CFO sign-off — which means almost every deal carries at least one person whose entire incentive is to find the reason this might go wrong. Multiply that instinct across a committee and the default isn’t caution. It’s paralysis.

Now add the people. The average B2B buying group is large and the counts disagree in a way that turns out to be the whole point: 6sense puts it near ten; Forrester’s 2026 figure reaches twenty-two once you include external influencers; another survey insists most groups are under five. These aren’t contradictions. They’re three different counts of three different things — and the disagreement is the finding. Nobody can say with confidence how many people are actually in the room. The boundary of the buying group is itself opaque.

Coordination debt, with a human face

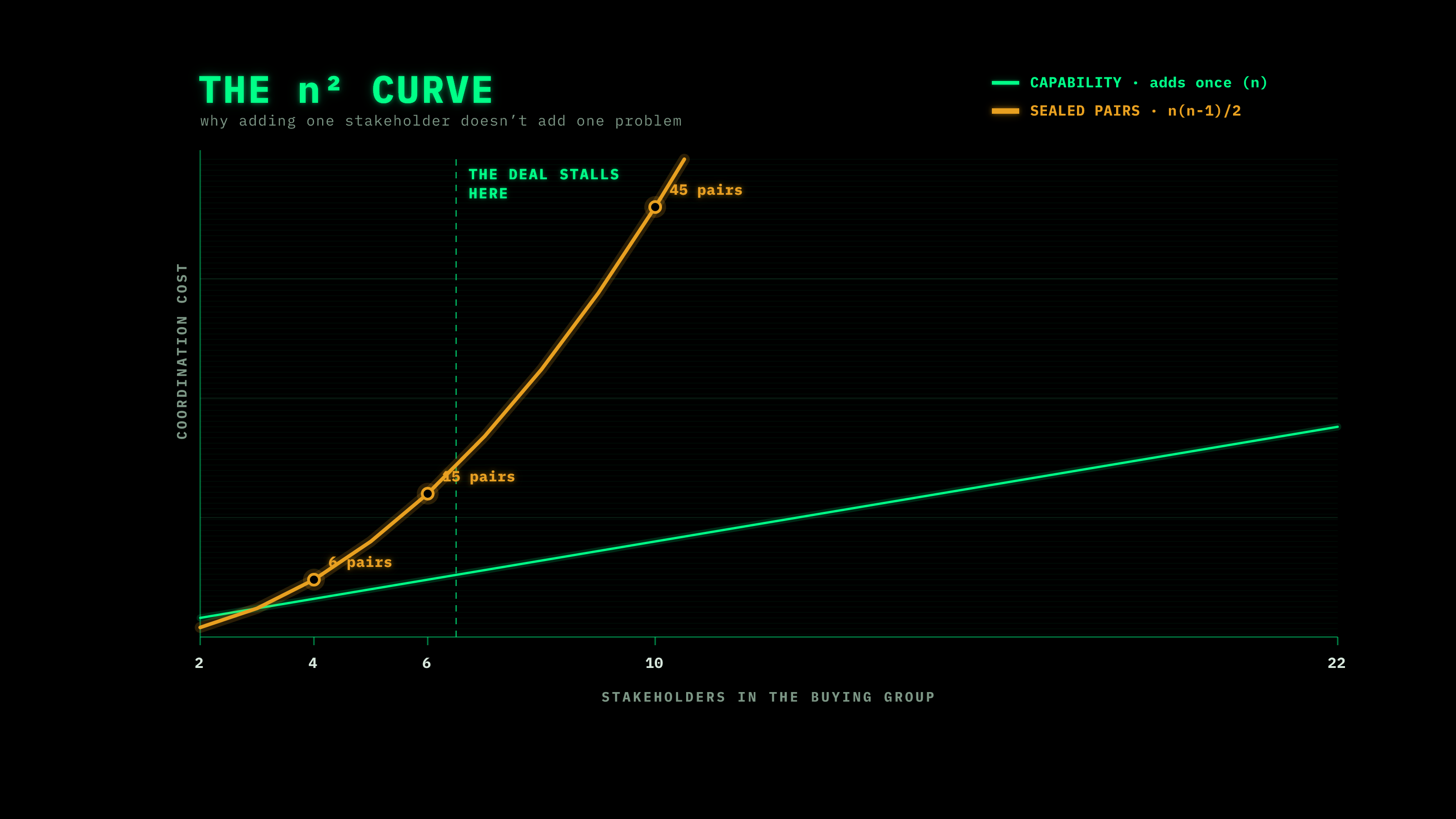

I’ve argued before that when agents can’t see into each other, every agent must maintain a predictive model of every counterpart it depends on — and that the cost of building and being wrong in those models grows with the square of the relationships. I called it coordination debt. It was a claim about software. It is also a claim about the room.

A buying group is a network of sealed peers. The CFO can’t see the security lead’s compliance exposure. Legal can’t see the CFO’s budget pressure. The champion can’t see what, exactly, will make the VP of Ops feel safe. Each stakeholder models what the others will accept, from interface declarations and behavioral history alone — which is to say, from meetings and guesses. The bilateral relationships in a group of n people number n(n−1)/2: order n². Capability — what each new stakeholder actually contributes to the decision — adds once, order n.

So the same law holds. Add a stakeholder and the group’s competence grows by one increment while the mutual-modeling overhead grows by the number of people already in the room. Four stakeholders is six sealed pairs. Add two more and you have fifteen. The guessing grew two and a half times faster than the expertise. Past some size, every additional voice in the room subtracts more confidence than it adds — and the path of least resistance, for everyone, is to not move.

FOMU is what that overhead feels like from inside a single head. The fear is real. But the fear is downstream of the topology.

The data has the signature

This is where the 2026 numbers stop being trivia and start being evidence. No-decision losses concentrate in exactly the place the structure predicts: large, cross-functional committees, where the sealed pairs are most numerous and the behavioral history thinnest. Single-decision-maker purchases mostly close — n=1, nothing to model, no coordination debt. The failures cluster where the n² wall is highest. Indecision shows up in roughly nine of ten complex deals; it barely registers in simple ones. That gradient is the fingerprint.

And like any claim worth making, it’s falsifiable. If coordination debt is what stalls these deals, the no-decision rate should rise superlinearly with the number of stakeholders in the committee — accelerating, not tracking a straight line. If your own pipeline shows no-decision rates climbing in step with committee size, linearly, the theory is wrong and you should discard it. Any RevOps team can run this against its own closed-lost data this quarter. I’d genuinely like to know what it shows.

What the structure prescribes

The instinct, when a deal stalls, is to manufacture urgency — to dial up FOMO, to make the cost of waiting vivid. The structure says this is precisely backwards. Adding urgency raises the stakes on a decision the group already can’t align on; you are pressing harder on a door that opens inward. More fear, of either kind, deepens the freeze.

What lowers coordination debt is not a sharper pitch. It’s reducing the cost of being wrong, for the whole group at once.

Equip the champion as a translator. Your champion has to carry your value into a room you’ll never enter, and re-explain it in the private language of each sealed peer — the CFO’s defensible business case, the security lead’s compliance answer, Legal’s rollback clause. Give them that language, pre-built, per stakeholder. A champion who can’t translate is a single point of failure.

Name the risks before the buyer does. The research is blunt here: implementation effort, not price, is the dominant reason buyers stay with the status quo — by a factor of roughly three to one. Dropping your price doesn’t make switching feel safer; proving the transition does. Put the rollback, the migration plan, the reference from a company that looks like theirs into the core narrative, not the appendix.

Spend the room’s confidence deliberately. You are not selling a product into a buying group. You are selling the group permission to agree — which means your real competitor is the version of them that does nothing, and your real job is to make doing nothing feel more expensive than moving.

The deal that died didn’t lose a comparison. It failed to resolve a network — a handful of people who couldn’t see into each other’s risk, each modeling the others, all defaulting to the one choice that required no one to be accountable.

The vendors who compound in the next few years won’t be the ones with the sharpest demo. They’ll be the ones who understood that the buying group is a sealed network, that fear is just the interest payment on its coordination debt, and that the whole game is helping a room full of strangers agree.

And the next turn is already visible: the buying group is about to include agents. AI procurement copilots, autonomous evaluators, the CFO’s analysis bot — more sealed peers, modeling each other, in the same room. The human version of this problem and the machine version are converging into one. I track that convergence weekly in KSI.

The Coordination Debt Audit

I built a one-page diagnostic to go with this piece: five falsifiable questions to score your own buying-group risk — the verification-call ratio, the committee-size trend in your no-decision deals, the translation gap your champion is carrying. Free, no email required. [Download the PDF below.]

Key figures referenced in this piece: ~40% of qualified B2B deals end in no decision (40–60% of all lost deals); ~79% of B2B purchases require CFO sign-off; average buying group ranges from ~10 (6sense) to 22 (Forrester 2026); implementation effort outweighs price ~3:1 as the reason buyers keep the status quo; indecision present in ~90% of complex deals.

KSI · Krein Signal Intelligence — published weekly. By Lapo Chirici.